7.5 Significancia de Parámetros

To determine whether the predictors introduced in a logistic regression model contribute significantly, the hypotheses must be tested:

\[ \begin{aligned} &H_{0}: \beta_{k}=0\\ &H_{1}: \beta_{k} \neq 0 \end{aligned} \] Fail to reject \(H_0\) would imply that there is insufficient evidence to claim that \(beta_k\) is different from zero. In other words, \(x_k\) is not statistically significant for the model in the presence of the remaining independent variables.

The Wald statistic is used to test these hypotheses.

\[W(\beta_k) = \dfrac{\hat\beta_k}{se(\hat\beta_k)},\]

where, if \(H_0\) is true, \(W(\beta_k)\) follows a Normal Distribution \(N(0,1)\) (also known as \(Z-\) test).

If the model has a single independent variable, the LLLR test can be used to evaluate \(H_0:\beta_1=0.\)

The confidence intervals for \(\beta_k\) can be estimated using a Normal Distribution. Thus an interval of \(100(1-\alpha)\) confidence for \(\beta_k\) is:

\[ \hat{\beta}_{k} \pm z_{\alpha / 2} se(\hat{\beta}_{k}) \]

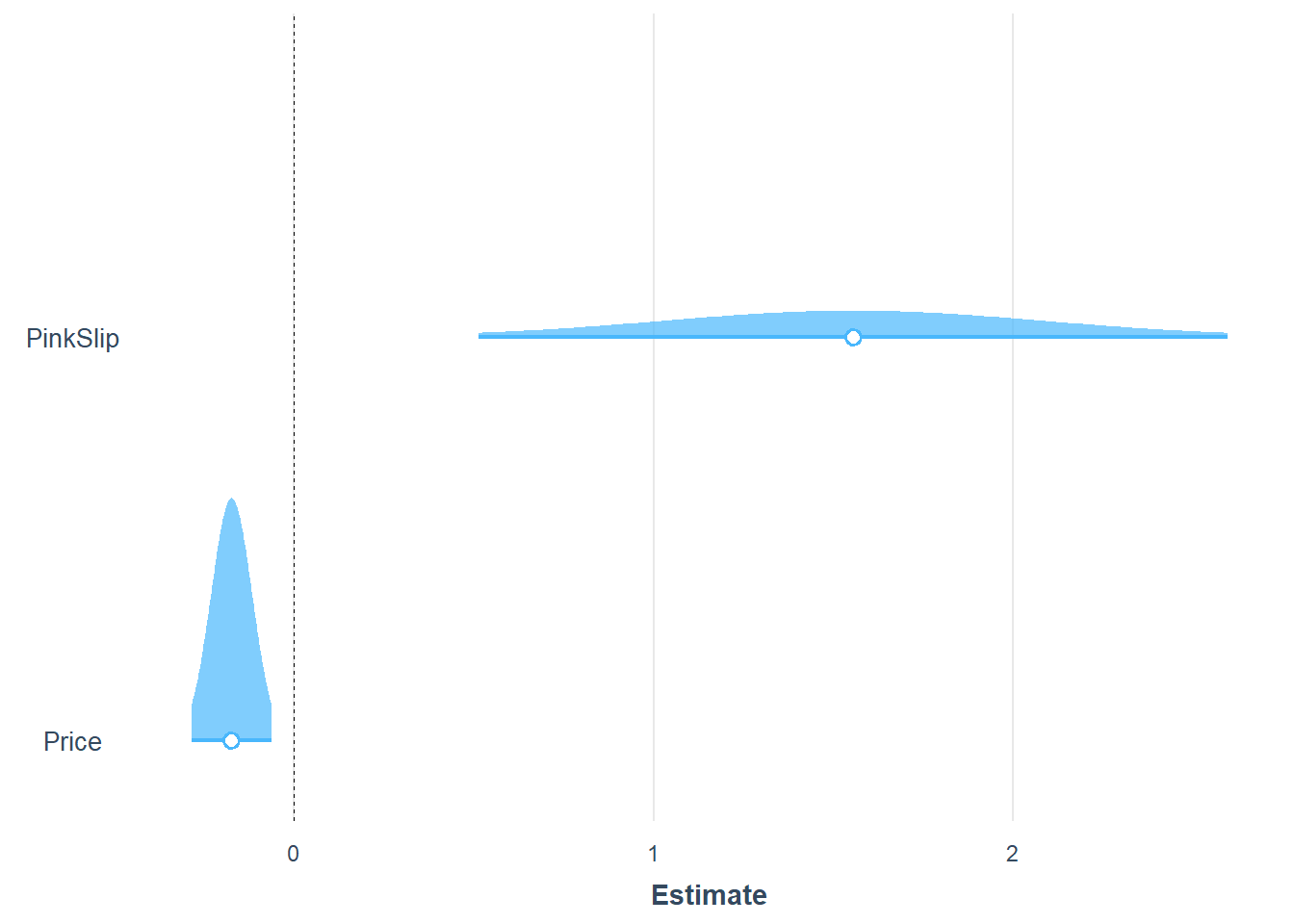

- In our example:

| Sold | ||||

|---|---|---|---|---|

| Predictors | Odds Ratios | std. Error | Statistic | p |

| (Intercept) | 1.49 | 0.71 | 0.82 | 0.410 |

| Price | 0.84 | 0.05 | -3.04 | 0.002 |

| PinkSlip | 4.73 | 2.52 | 2.93 | 0.003 |

| Observations | 100 | |||

| R2 Tjur | 0.185 | |||