16 Smoothing Methods

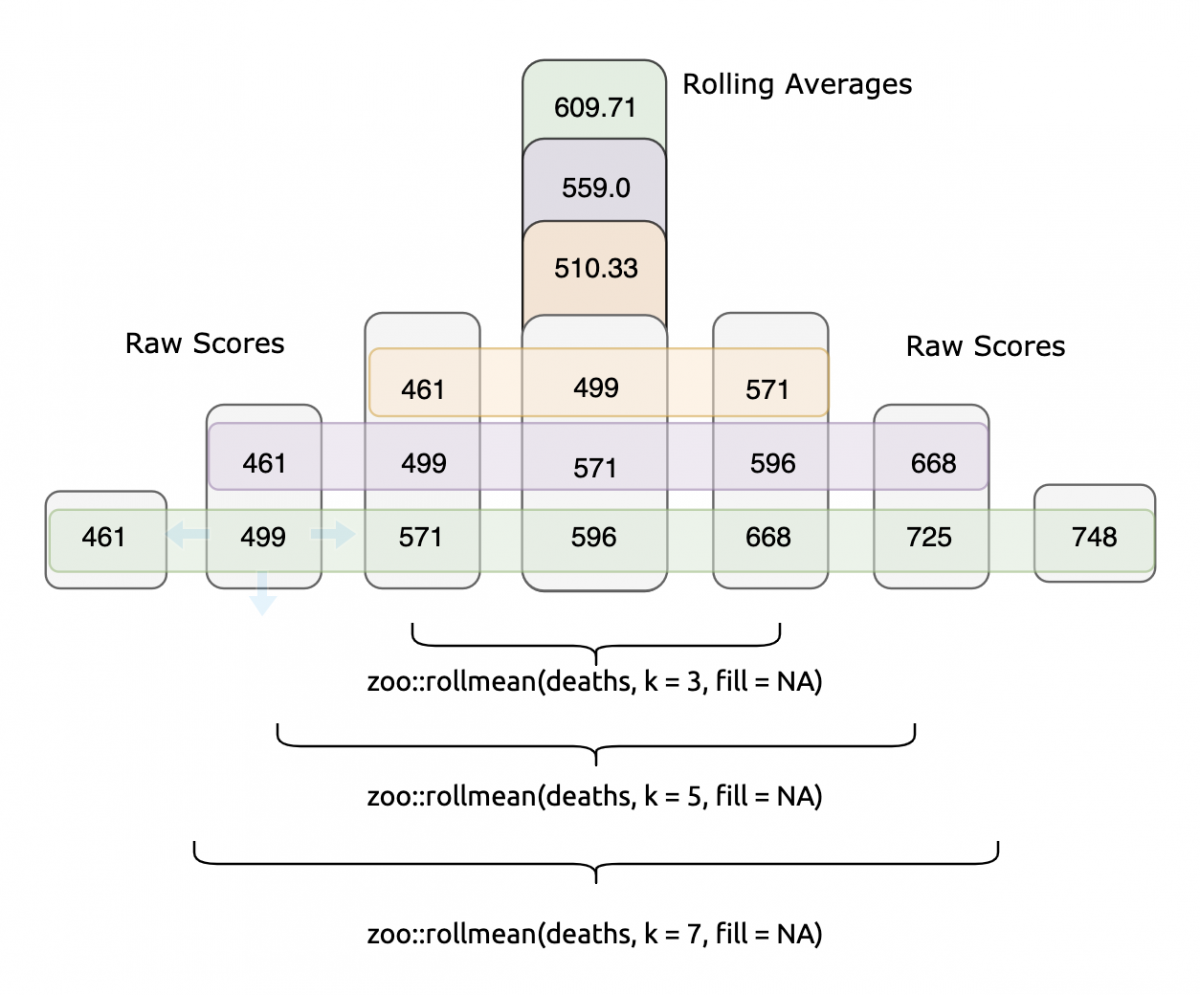

Moving-average forecast models use the average of the last \(k\) observed values to forecast next period’s value. The number \(k\) is called the span of the moving average. Larger values of \(k\) result in a smoother model.

The forecast equation for the simple exponential smoothing model is a weighted average of last period’s observed value and last period’s forecasted value. The degree of smoothing is determined by the choice of a smoothing constant \(w\) . Some practitioners restrict \(w\) to the range of \(0\leq w \leq 1\), but some software will allow for a range of \(0 \leq w < 2\).